Australia has a growing hedge fund industry, but the main hedge fund centres remain London and New York. While Australia has the largest amount of hedge funds under management in the region (recently estimated at $40 billion), a respected regulatory regime and high quality people, it is Hong Kong, Singapore and possibly Tokyo that are vying for hedge fund leadership in Asia.

What would it take to set Sydney on a path of hedge fund leadership in the region?

The key stumbling block is tax, in particular withholding tax. While other jurisdictions have strong records in providing hedge fund services the main advantage they carry over Australia is tax. A number of centres, such as the Cayman Islands, Bermuda and British Virgin Islands have established a strong position in servicing hedge funds by offering a tax-free environment for investors and managers. Other developed markets such as the UK, Ireland, Luxembourg, Hong Kong, and Singapore do not impose withholding tax and market this as a key selling point in attracting foreign direct investment.

So what is the logic of withholding tax? Withholding taxes such as PAYE in Australia are designed to limit avoidance and evasion by taxing at the source of income. Withholding tax on non-residents however does not carry the same logic, except to reduce the opportunity for residents to configure their arrangements to appear to be non-residents and avoid domestic taxation. Applying withholding tax on non-residents is a case of cutting off our nose to spite our face; it may be effective in reducing avoidance activities of residents, but it is also effective in turning away genuine non-residents and spurning the development of an Australian hedge fund industry.

Withholding tax has the effect of securing taxation revenue from a small domestic hedge fund industry, but prospective taxation revenue on a new regional or global industry is foregone. Let me explain.

Currently, overseas investors in Australian hedge funds (and investments generally) are subject to withholding tax. While withholding tax is also applied in many countries that might compete with Australia for investors, there are other well-established jurisdictions that do not impose withholding tax and are thus in an advantaged position to offer hedge fund products.

Thus, to meet overseas demand for Australian hedge funds, Australian managers generally develop and offer hedge fund products by way of an offshore-based fund company registered in such jurisdictions as the Cayman Islands. Generally, investment management is conducted by an Australian investment manager team either directly or by way of an advisory agreement with the fund company, although in some cases fund managers are incentivised to set up their entire businesses overseas. In any case, the related services of custody, prime broking, administration, legal, accounting and audit are generally delivered by overseas-appointed providers.

For offshore structured Australian hedge funds, the Australian government does participate in the taxation revenue associated with a fund's earnings remitted to Australian participants. However, there is a substantial leakage of revenue from the absence of withholding tax (because the funds are not located in Australia) and both individual and corporate taxation proceeds from Australian service providers that are NOT being used by the overseas fund company. The Australian government will earn withholding tax on those investors who do choose to invest in Australian products despite the disadvantages of doing so. Withholding tax thus has the unintended impact of shackling jobs growth and lowering potential taxation revenue.

To be a centre for hedge funds, Australia needs to attract all the ancillary hedge fund service providers and to provide an environment that would encourage both Australian and overseas fund managers to set up in Australia rather the current situation of encouraging Australian fund managers to set up overseas. Hedge fund managers are not constrained to investing in domestic assets and so the domicile of a hedge fund business will be driven by factors such as tax, people and regulator.

The BOLD decision would thus be to remove withholding tax on all non-resident financial asset investments in Australia based on the expectation that the withholding tax forgone will be more than outweighed by higher corporate and individual taxation associated with increased exports of financial services and greater jobs growth and of course the collection cost of the withholding tax. Modelling this analysis would be a very worthy exercise.

The application of withholding tax is particularly inappropriate in the case of funds offered to overseas investors that invest primarily in overseas assets in what the authorities term "non-Australian things".

Thus, a SECOND BEST solution is to acknowledge that the current policy to tax Australian-sourced income regardless of residence of the investor will not change. In this event, we should accept that Australia will NEVER be a regional funds management centre and instead look to particular areas where Australia can grow the hedge fund industry on the margin to the mutual benefit of government and industry.

Australian fund managers investing in “Australian things” will continue to require an offshore structured fund company for overseas investors, and if warranted by demand from Australian investors a second fund with Australian service providers as Australian investors are limited by FIF in their investments in offshore fund companies. While this twin structure is costly and inefficient, it is the only practical way to proceed in these circumstances.

However, where a fund’s investors are exclusively non-resident and activities are principally related to “non-Australian things” these non-residents investors should be exempt from a withholding tax to allow Australian fund managers to compete globally.

For clarity, the fund should not be denominated in Australian dollars, Australian FIF rules should not apply, foreign exchange contracts would be permissible provided they were in respect of overseas assets and management fees would be taxable at the company tax rate.

To tackle the additional risk of avoidance by residents, the exemption could be set to only apply to those non-residents of tax treaty countries including on a “look through” to the ultimate holder of a trust.

Australian non-resident withholding tax is a material impediment to potential growth of the hedge fund (and financial services) industry in Australia. In view of the other advantages Australia carries in financial services, exempting non-residents from withholding tax (with some reasonable caveats) would take Australia to a position of regional leadership in hedge funds.

Friday, August 25, 2006

Friday, August 18, 2006

Participants in the Australian Hedge Fund Industry

The Australian hedge fund industry is young, but growing quickly. There are a number of hedge fund managers delivering single and multi-strategy products as well as aggregators offering fund of fund products. However, the available information on the make-up of the participants is sketchy.

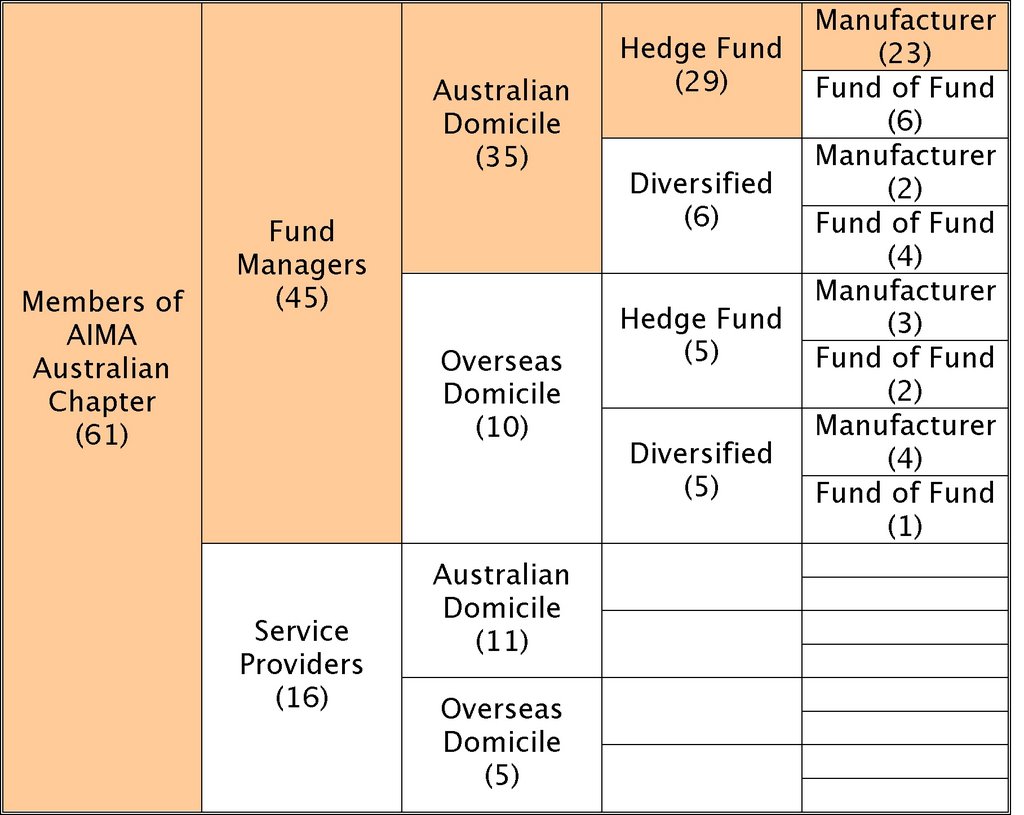

The Australian hedge fund industry is young, but growing quickly. There are a number of hedge fund managers delivering single and multi-strategy products as well as aggregators offering fund of fund products. However, the available information on the make-up of the participants is sketchy.The attached table examines the membership of the Australian Chapter of AIMA and dissects members according to some key criteria.

There are in excess of 1,000 members of AIMA globally and 61 (6%) members in the Australian Chapter. This is higher than Australia's weight in global sharemarkets for example. While there will be hedge fund managers who are not members of

AIMA, using this membership as a proxy for the industry as a whole in Australia shows some interesting results.

The first split shown is between fund managers (74%) and service providers (26%) such as lawyers, custodians, brokers and exchanges. Of the fund managers, 78% had their primary domicile in Australia and the balance overseas. Among the Australian domiciled managers, 83% were special purpose hedge fund managers and the others part of a diversified financial services business. Finally, 80% of hedge fund managers manufactured funds while the balance aggregated fund of funds.

In summary, of the 61 members of the AIMA's Australian Chapter, 23 (38%) are hedge fund manufacturers. These managers provide product for Australian retail and institutional investors, and in some cases overseas investors by way of special purpose vehicles or mandates.

Thursday, August 17, 2006

Australian Superannuation Funds Use of Hedge Funds

The assets of Australian Super funds total around $1 trillion and, despite the value of hedge funds in portfolio construction, have less than 3% invested in this asset class.

The University of NSW and the Australian chapter of AIMA conducted a survey in Jan 2006 aimed at examining the attitude of Super funds to hedge fund investing. The respondents to the survey carried funds under management of more than A$145 billion.

The key findings of the study were:

The University of NSW and the Australian chapter of AIMA conducted a survey in Jan 2006 aimed at examining the attitude of Super funds to hedge fund investing. The respondents to the survey carried funds under management of more than A$145 billion.

The key findings of the study were:

- current allocation of under 3% is expected to rise to over 4% over the next 2-5 years

- the current focus on global strategies is expected to remain - surprisingly only 14% were Australian-based strategies

- funds of funds represented 49% of investments, although this is expected to decline in favour of individual funds and multi strategy funds in future

- the most popular strategy is long/short equity

- operational and governance issues were most important to those considering investment

Tuesday, August 15, 2006

Australia's ASIC Studies Hedge Funds

Australia's financial services regulator, ASIC, is researching hedge funds in Australia to better understand the potential risks to investors. The study, based on publically available information, will not be published and will be used for internal purposes only.

In Australia, hedge funds may be offered to retail investors under a registered Product Disclosure Statement. Around half the A$20 billion Australian hedge fund industry is made up of registered funds.

A key observation of the study is that the funds offered are more benign then ASIC had expected in a number of respects; gearing, fees and profitability.

Also, there does not appear to be any disruptive influence by foreign-operated hedge funds on the efficient and proper functionaing of Australian markets.

As with all funds offered to Australian investors, ASIC is concerned that product documentation needs to be "clear, concise and effective". Hedge funds are not likely to be singled out in particular compared with other retail/mutual funds.

In Australia, hedge funds may be offered to retail investors under a registered Product Disclosure Statement. Around half the A$20 billion Australian hedge fund industry is made up of registered funds.

A key observation of the study is that the funds offered are more benign then ASIC had expected in a number of respects; gearing, fees and profitability.

Also, there does not appear to be any disruptive influence by foreign-operated hedge funds on the efficient and proper functionaing of Australian markets.

As with all funds offered to Australian investors, ASIC is concerned that product documentation needs to be "clear, concise and effective". Hedge funds are not likely to be singled out in particular compared with other retail/mutual funds.

Monday, August 14, 2006

What is a hedge fund?

The two defining features of a hedge fund are leverage and short selling. While traditional funds managers may also leverage and short sell they are generally conducted more extensively by hedge funds. There are other differences like fees, transparency of process and regulation which I will address in later posts.

Subscribe to:

Posts (Atom)